If you’re staring at a pile of balances and wondering where to begin, you’re not alone. Choosing a debt payoff method feels like picking a path through fog — both lead forward, but one might get you across the clearing faster while the other keeps you steadier on long slopes. This post breaks down the two most popular approaches in plain language, with real-world considerations so you can pick the one that fits your life — not some spreadsheet’s ideal.

Quick definitions (the TL;DR)

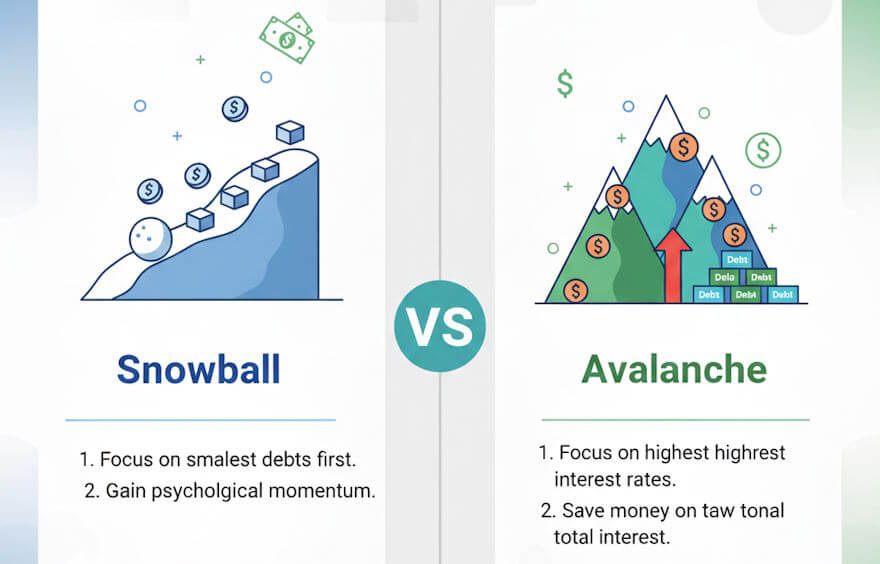

Debt Snowball: Pay off your smallest balance first while making minimum payments on the rest. When the smallest debt is gone, roll that payment into the next-smallest balance — like a snowball gathering size and momentum.

Debt Avalanche: Prioritize debts with the highest interest rates first, paying them down aggressively while meeting minimums on others. This minimizes the total interest you pay over time.

Numbers vs. psychology: why both matter

On paper, the avalanche almost always saves you money. Less interest, fewer months, and — if you like crisp financial math — it’s an easy choice. But humans aren’t spreadsheets. Motivation, momentum, and mental health play enormous roles in whether a plan actually gets followed.

For some people, the snowball’s psychological wins — quick small victories and visible progress — create sustainable momentum. For others, the avalanche’s efficiency and comfort of knowing you paid the most expensive debt first bring peace of mind. Your personality, life circumstances, and how you reward yourself all matter.

When the real world interferes

Modern borrowers juggle more than just balances: irregular income, family emergencies, and occasional financial shocks change the landscape. Consider someone paying down credit cards while navigating medical bills, or a freelancer whose cash flow fluctuates month-to-month. In those cases, a plan that’s forgiving and confidence-building can be more valuable than the absolute cheapest route.

Also — and this is worth a quick, practical mention — certain service experiences can push people into urgent debt decisions. For example, members sometimes worry about whether late payments to gyms or subscription services will trigger collections. If you’re researching that topic, you may come across resources about Planet Fitness and debt collections, which illustrate how seemingly small debts can go sideways if they’re not handled in time.

Head-to-head comparison

Below is a handy table to help you compare the approaches at a glance.

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| Primary focus | Smallest balance first (psychological wins) | Highest interest rate first (math wins) |

| Average time to payoff | Often longer if interest rates are high | Often shorter — minimizes interest over time |

| Emotional impact | High motivation from quick wins | Less frequent wins, but steady financial improvement |

| Best for | People who need behavioral momentum | People who are disciplined and want to minimize interest |

| Complexity | Simple to implement | Requires tracking rates & sometimes recalculating priority |

How to choose: three practical rules

- Start where you will actually start. If staring down high-interest cards makes you freeze, begin with a tiny balance and build confidence. If numbers motivate you, go avalanche and save on interest.

- Combine the tactics when needed. There’s no rule that says you must be religiously pure. Some people pay the smallest balance each month while putting an extra amount toward the highest-rate card. Hybrid approaches often balance psychology and math.

- Protect your baseline. No payoff plan works if you have no emergency fund. Build a small cushion (even $500–$1,000) so one surprise expense won’t blow up your progress.

Real-world example

Imagine Maria has three debts: a $600 store card (18% APR), a $3,200 credit card (24% APR), and a $12,000 personal loan (8% APR). She can afford an extra $400 per month beyond minimums.

If Maria picks the snowball, she pays off the $600 store card quickly — a morale boost that helps her keep going. If she picks the avalanche, she targets the 24% card and saves more in interest, but the first few months might feel less satisfying.

Both paths will eventually wipe the slate clean — the right one is the one Maria will stick to.

Tips that help either strategy work better

- Automate minimums and your extra payment so you don’t skip a month.

- Track progress visually — a simple paid-off list or a progress bar can be hugely motivating.

- Consider small, planned rewards when you hit milestones (non-monetary or low-cost treats reduce the urge to derail).

- Revisit your plan after life events — promotions, new kids, or medical bills may require adjustments.

- When possible, negotiate interest rates or move balances to a 0% introductory transfer — but read the fine print.

When to get help

If debt feels overwhelming — you’re getting collection notices, wage garnishments, or you suspect identity theft — talk to a certified credit counselor or a trusted financial advisor. Free and low-cost nonprofit credit counseling agencies can help you make a realistic plan and sometimes negotiate with creditors on your behalf. If legal risk is present, consult a consumer attorney in your area.

Final thoughts

There is no one-size-fits-all winner. The avalanche is mathematically superior in most cases, but the snowball often wins the human race because humans need encouragement as much as efficiency. Pick the approach that fits your temperament and life context, automate what you can, build a small emergency buffer, and measure progress in months and morale — not just dollars saved.

At the end of the day, the best strategy is the one you can stick with. If that means choosing small, frequent wins today to build the discipline that lets you tackle the rest tomorrow, that’s a smart choice.